As lockdown restrictions lift across the UK, there are many things to consider when booking a holiday which can seem overwhelming. One huge consideration is that there’s uncertainty still remaining around travel cancellations, vaccinations and which countries will be open to tourists. You’ve no doubt heard horror stories about unfortunate individuals whose holidays got cancelled and then they weren’t able to get a refund.

All of this means it’s more important than ever to know your rights and be savvy when booking your next trip. In this blog we are going to tell you about your Chargeback and Section 75 rights, which in simple terms are the rights you can use to claim money from your debit or credit card provider if a company you bought from refuses to refund you. We’ve also included a round up of the most popular travel money cards alongside the kind of protection they offer.

An important thing to remember is prevention is always better than cure. To prevent getting into a situation where a retailer is refusing to refund you, ensure you check the T&Cs of any big purchases, book direct with providers and limit your use of cash when abroad so you can use the protection offered by your debit or credit card provider.

When should I use Chargeback?

Read this section if…

You’re trying to get a refund on a purchase you made with your debit card

You’re trying to get a refund on a purchase you made with your credit card that is valued at under £100

Currensea travel debit card

What is Chargeback?

Chargeback is a consumer protection scheme - managed by your card provider - that is there to protect credit and debit card purchases, allowing cardholders to put in a claim for a refund from the business they bought from in reaction to a number of different eventualities; including if the goods are damaged, are not as described, haven’t been ‘delivered’ or if the merchant has ceased trading.

How do I apply for Chargeback?

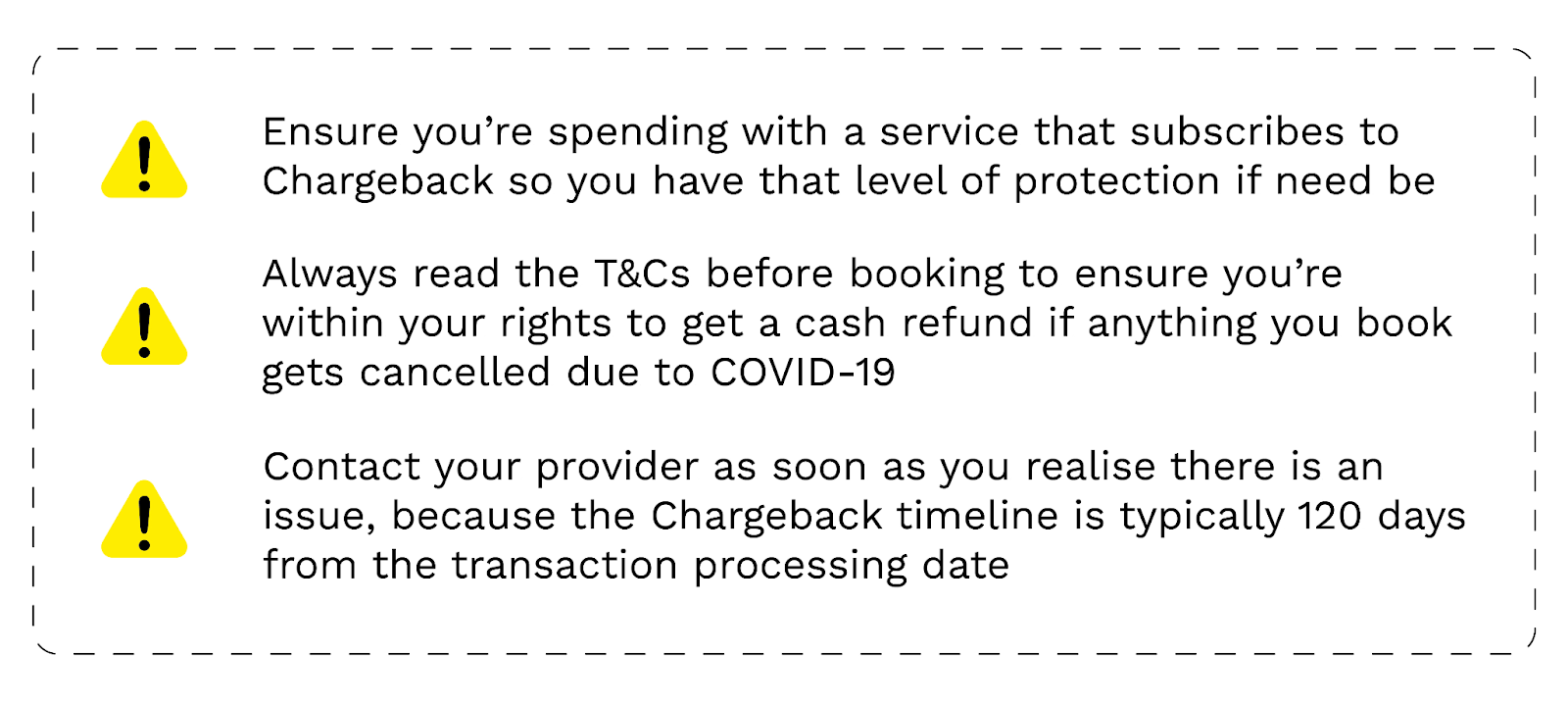

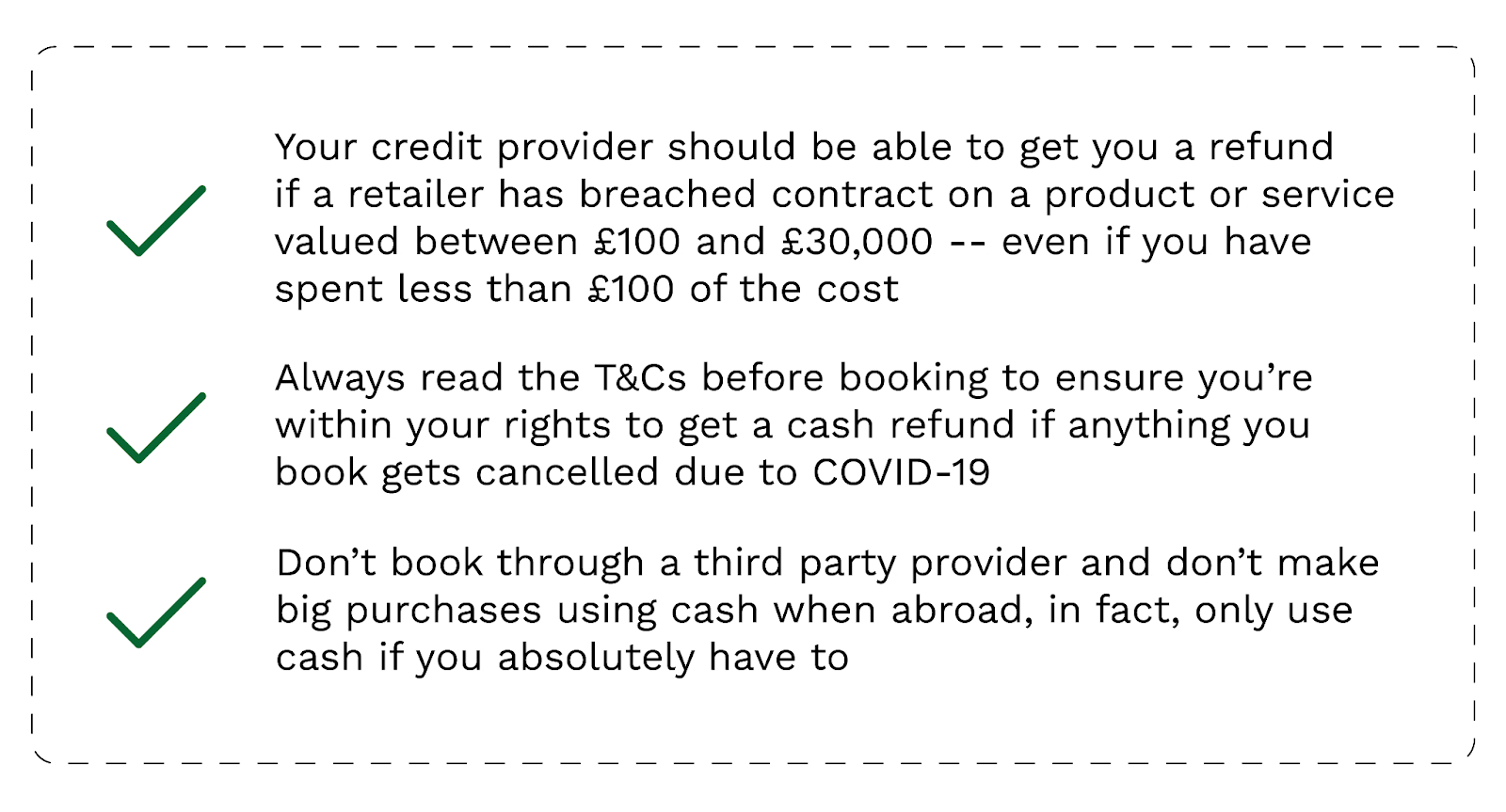

So, if you’ve had a flight, holiday or hotel cancelled due to COVID and the company is refusing to pay you back, how do you know if you can request Chargeback? First, check the T&Cs of your booking - ahead of booking any travel at the moment this is more important than ever because unfortunately if the T&Cs say “no refunds”, “transfers only” or have it in writing that they will only refund customers in voucher form, you will not be able to claim Chargeback. If the T&Cs don’t say any of the above you are within your rights to claim Chargeback.

Chargeback isn’t law, but rather is part of what is known as Scheme Rules, which only some participating providers subscribe to, so you need to make sure your card provider is on the list to protect yourself. Luckily all the big players i.e. Visa, Mastercard and American Express all subscribe so if you’re using a popular card you should be protected.

When you’re ready to make a claim, get in touch with the card provider as soon as you can because there is a typical time limit of 120 days on Chargeback claims. Contact your card provider via phone to speak with a customer services representative who should be able to advise you on next steps or you can use this really helpful claim form from Which? that guides you through the process.

What do I do if my card provider can’t help?

Unfortunately, traders can sometimes find ways to show you’re in breach of contract for not paying (another reason why being really careful with T&Cs is important) and your provider may not be able to refund you. If you believe you’re within your rights but your provider can’t help, you can ask for something called a letter of deadlock (template from Citizens Advice here) and contact the Financial Ombudsman Service who will escalate the problem.

The important learnings from this section are:

When should I use Section 75 of the Consumer Credit Act?

Read this section if…

You’re trying to get a refund on a purchase you made on your credit card valued over £100 and under £30,000

What is Section 75?

The catchily named Section 75 is a really important consumer protection right meaning your credit provider is liable if something goes wrong with something purchased from a retailer using credit, for example if the trader has gone out of business or isn’t responding to your emails or calls.

Section 75 is actually one of the big benefits of using a credit card whenever you make a big purchase, because it means you have guaranteed protection. However, if you’ve checked that your provider is subscribed to Chargeback (like Currensea is!) you also have this same protection when spending with your debit card.

How do I make a Section 75 Claim?

To make a Section 75 claim, the value of the purchase must be over £100 and not more than £30,000. Now comes the confusing bit so we’ll try to keep it simple! Even if you spent under £100 on your credit card, it’s the value of the whole purchase that matters. So let’s say you spent £80 on a deposit for a hotel stay and the hotel is trying to invoice you for the entire stay of £800. Even though you only spent £80, you can make a Section 75 Claim because the entire value of the product is £800, so over £100.

Next, we probably sound like a broken record if you read the Chargeback section, but… T&Cs! Go back and read the T&Cs to check that you’re within your rights to a refund (i.e. the provider hasn’t written “no refunds!” in the T&Cs you signed). On top of this - and this is really important for travellers like us - if you paid through a third party company, like a bookings website or package holiday provider, Section 75 may not apply. This is because your credit card provider could argue you didn’t make the purchase directly to the supplier you are looking for a refund from, which is compulsory for Section 75 claims.

Again, to make a Section 75 claim call your credit provider or use the good old Which? claim tool.

What if I paid in cash, but took the money out of an ATM using my credit card?

Unfortunately, Section 75 doesn’t apply if you paid in cash (even if the cash came from your credit card) because your credit provider will have no record of a link to the service you purchased from. If you need cash on holiday, take the exact amount you need out of an ATM using a Currensea card to avoid being hit by big fees. We recommend using your Currensea purchases abroad that have a card payment option to ensure you’re protected… and to guarantee the best savings!

What do I do if my credit provider can’t help?

The really annoying thing about Section 75 is that there is no timeframe on when your credit company needs to resolve the claim, so if it’s taking ages we recommend contacting the Financial Ombudsman Service using a letter of deadlock (template from Citizens Advice here) which will allow you to escalate the claim.

The important learnings from this section are:

So, what are my rights with different cards?

Hopefully you’re never in the position where you need to use your Chargeback rights or Section 75, but with all of the cancellations going on in the travel industry right now, it makes sense to pick a provider that you know will have your back. We’ve had a look at some of the top methods of spending abroad (the top five are all included in MoneySavingExpert’s round-up of the best travel spending cards) to check what your rights are so it’s easy for you to pick the best choice for you...

Comparing your rights with the leading travel spending methods

Further reading

Here are some links to some great articles with further information should you require it…

- https://www.ukfinance.org.uk/faqs-chargeback-rights-and-section-75-and-coronavirus

- https://www.money.co.uk/guides/chargeback-claims-how-to-get-your-money-back.htm

- https://www.moneysavingexpert.com/reclaim/visa-mastercard-chargeback/

- https://travelweekly.co.uk/articles/367301/advice-what-you-need-to-know-about-chargebacks-and-section-75-of-the-consumer-credit-act

- https://www.fca.org.uk/publication/finalised-guidance/cancellations-refunds-helping-consumers-rights-routes-to-refunds.pdf

- https://www.chargebackgurus.com/blog/airline-and-travel-agency-chargebacks

- https://www.which.co.uk/consumer-rights/advice/how-do-i-use-chargeback-abZ2d4z3nT8q

- https://www.which.co.uk/consumer-rights/regulation/section-75-of-the-consumer-credit-act-aZCUb9i8Kwfa

- https://www.fca.org.uk/consumers/coronavirus-cancellations-getting-refund-claiming-insurance